The views expressed are those of the author at the time of writing. Other teams may hold different views and make different investment decisions. The value of your investment may become worth more or less than at the time of original investment. While any third-party data used is considered reliable, its accuracy is not guaranteed. For professional, institutional, or accredited investors only.

At Wellington for the past several years, we have worked in partnership with asset-owner clients to help them implement their net-zero goals in actively managed equity and corporate credit strategies. For most clients, the primary challenge when implementing these goals is balancing their decarbonisation ambitions with their financial return objectives. To meet this challenge, defining robust guidelines is, in our view, a key step in setting mandates up for success across clients' climate transition as well as financial objectives.

For those clients who have requested implementation of a decarbonisation glidepath in the portfolios we manage on their behalf, we work with them to strike the right balance for their organisation and to formulate tailored guidelines using sensible metrics and high-integrity implementation. Here, we share some of the notable lessons learned.

KEY POINTS

For asset owners seeking to implement net-zero goals successfully within their investment strategies, we recommend a tailored, five-step approach:

- Tailor the decarbonisation target to the investment mandate

- Lean into what active managers do best: fundamental research and engagement

- Utilise forward-looking and nuanced metrics

- Assess the scope(s) of the ask

- Draft clear guidelines with minimal room for (mis)interpretation

To help asset owners implement these key lessons learned, we provide a sample template at the end of the paper, which sets out the criteria we find most useful for defining a decarbonisation glidepath.

1. Tailor the decarbonisation target to the investment mandate

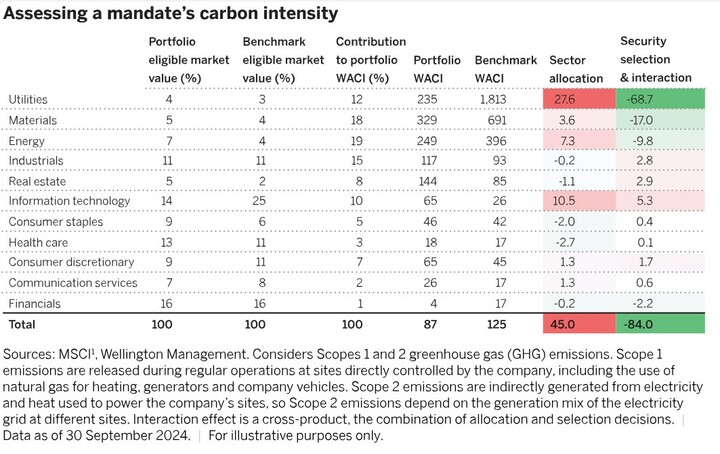

While it may seem obvious, different investment universes and styles have different starting points in terms of transition metrics. With this in mind, we typically start by assessing the data coverage of the opportunity set, which is highest across equities and corporate credit. We then look at benchmark-relative or absolute contribution to understand the carbon intensity of the mandate. We have selected weighted average carbon intensity (WACI) as the preferred portfolio metric our investment teams will monitor and target for the interim 2030 decarbonisation target, as we find it less sensitive than other portfolio metrics, such as financed emissions, to changes in the market and capital structures. For benchmark-relative mandates, we can use two-factor attribution to assess how much of a portfolio's carbon footprint comes from sector allocation and how much comes from security selection. The example in Figure 1 compares a global, value-orientated equity portfolio with its global, core benchmark.

Figure 1 shows that the portfolio is overweight the most carbon-intensive sector, utilities. However, the utilities stocks held in the portfolio are less carbon-intensive than the average within the sector.

Attribution is most often used for point-in-time analysis. Some mandates, particularly those that are opportunistic or less benchmark sensitive, may experience significant fluctuations in carbon performance over time. When considering the appropriate pace for a WACI glidepath, we often use sensitivity analysis to assess the impact of prospective high-conviction investment decisions on WACI.

Assessing the carbon intensity of specific mandates provides deeper insight and line-of-sight for asset owners about how portfolios will perform over time and interact with proposed target thresholds. For example, if the same portfolio from Figure 1 leaned into utilities holdings with higher carbon intensity today and engaged with those companies to enhance their transition plans, the current portfolio WACI could increase substantially, at least in the short term. This may be consistent with the philosophy and process of the investment team and may be a desired outcome for the asset owner. Crucially, we seek to avoid any investment-style "creep" because of a climate objective and, instead, maintain a consistent fundamental role in our clients' portfolios.

2. Lean into what active managers do best: fundamental research and engagement

As an active manager, we believe constructive dialogue with companies can be a powerful tool to achieve better investment outcomes for our clients. These discussions can help portfolio companies appreciate the potentially wide-ranging effects of the low-carbon transition on security valuations. Company meetings can also help certain investment teams better understand a business's emissions footprint and transition risk-management approach. Where transition risk is material to the company, we aim to highlight this risk and encourage risk mitigation.

As more company management teams appreciate the contribution of a robust transition risk-management strategy to long-term financial success, the investable universe of climate-ready companies is likely to expand. This trend is supportive for active managers, who can then consider transition alignment on an equal footing with other factors in their investment process.

To read case studies about our engagement on climate-change risks and opportunities, see Section 3 of Wellington's TCFD-aligned Climate Reports.

1Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties herby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including loss of profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI'S express written consent.