Chris Parker, Head of UK Institutional Sales, Man Group

Becoming a retiree no longer means giving up investment risk. In this context, diversification is more essential than ever, argues Chris Parker.

Until a decade ago, almost all retirees swapped a lump sum for a regular fixed payment, or annuity. For pension providers, that meant targeting investments towards annuity rates. Owning gilts (whose yields are linked with annuity rates) and eventually, ‘risk-free' cash, was enticing.

Since the UK Government's Freedom and Choice reforms in 2015 and the FCA's Investment Pathways six years later, retirees have been encouraged to think about how their retirement needs will change through their active years, later years, rainy day funds and legacy planning.

They may now withdraw their tax-free cash, buy an annuity or enter decumulation – or some combination of the three. Alternatively, they may stay invested, extending their investment horizon several decades.

With an increasing array of options for and expectations of pension savings, giving up investment risk isn't desirable – or even doable – for today's active retirees. However, managing risk and diversification is more important than ever, as I discuss below.

No risk, no reward

I should start by saying that annuities are not off the table and may still make sense for some people. So why have we seen such a large decline in take-up? One reason is that – recent higher interest rates notwithstanding – annuity rates remain low versus history (on a thirty-plus year view). As such, annuities are expensive to purchase. Secondly for those that can afford them, there is a sense that they don't feel ‘risk free'. Rather than taking investment risk, savers are making a longevity estimate about their own lives. The evidence suggests that retirees prefer to have the potential to leave something behind for loved ones.

Once the decision has been taken to keep at least some of a pension pot invested, the reasons why portfolio diversification and risk management remains so important in the run-up to retirement and beyond are quite intuitive.

First, there's the simple impact of time. After a market downturn, a 22-year-old saver has many more years of contributions and investment returns to smooth out the effect than a saver who is 62. They also benefit from compound interest (the booster effect of earning interest on previous interest), which we know is driven by the frequency and volume of interest-collecting periods. They have more opportunity to build gains, as they simply have more periods left for their savings to multiply.

Secondly, losses, like gains, have a way of adding up. ‘Volatility drag' acts like a tax in difficult markets and should incentivise prudent risk management. Put simply, if a 20% drop in markets after a £10 investment leaves a saver with £8, a subsequent 20% rise won't restore them to their initial sum – they will have £9.60. Short, sharp, volatility is seldom desirable, especially in retirement.

Risk shouldn't be a dirty word

Investment risk is not just a potential downside to manage – it is also a critical input to enable the continued growth of a healthy portfolio. It's widely accepted that savers should add investment risk in their ‘growth phase' by allocating to equities, before potentially switching to bonds and cash. However, an increasing number will want to generate more income after retirement – requiring the flexibility to dial up equity allocations again, or retain a high allocation to them, to and through retirement.

The simple fact though is that more equity risk comes with greater volatility and investment drawdown potential. For those close to or in retirement there is a risk the member will deplete their pot at a faster rate without having the time and contributions to recover these losses.

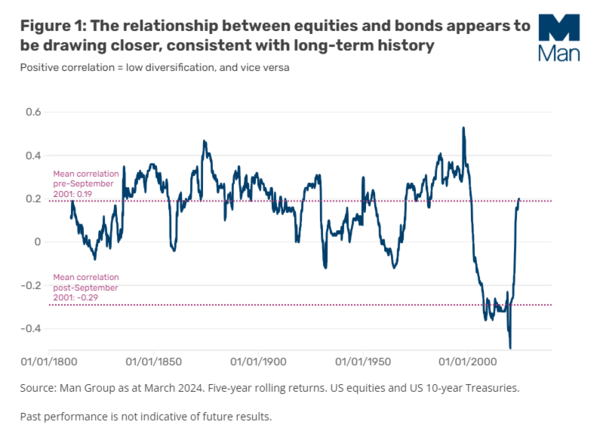

In this context, gilts are no longer a golden choice. Quite besides the fact that targeting annuity rates is now less relevant, data suggests we are entering a regime where the relationship between equity and bond returns is closer. Savers may not be able to lean on bonds to provide the protection they used to.

As we've written before, many schemes are turning to illiquids for growth potential and in many cases diversification. While there's no doubt a place for these in portfolios, achieving the theoretical diversification investors seek can be difficult in practice. They can exhibit a high correlation with equities and the same illiquidity premia which boost returns also present a challenge for precise rebalancing owing to their valuation lags. After retirement, schemes should ask if it makes sense to lock up soon-to-be retirees' capital at a time when they need liquidity the most.

Investment flexibility in retirement

To us, diversification and the ability to realise those gains, i.e. liquidity, are two sides of the same coin in investing, and this is especially true for DC members in retirement. Once retirees stop contributing, liquidity is paramount. This applies in normal markets in order to deliver precise rebalancing. It also holds during extreme drawdowns, where savers need to be able to sell assets to fund living costs and re-allocate.

A proper focus on risk management by investing in truly uncorrelated assets should in practice smooth the portfolio's returns profile. At Man Group, we feel that applying alternative investment techniques using the most liquid instruments across the main asset classes can provide these diversification and liquidity benefits. And if you invest in a combination of multi-asset liquid alternatives, retirees may not need to accept the lower returns profile which gilts offer. Savers may be able to take more equity risk and potentially generate a higher income the entire way through the glidepath, including after retirement.

Conclusion: Dynamic risk for active lives

With retirees now living longer ‘active' lives, we believe they should see their pensions investments as living investments, where risk should continue to be carefully managed, not static lump sums to crystallise. Simultaneously, savers should be cognisant of potential stumbling blocks such as volatility drag and sequencing risk. In this light, allocating to liquid alternatives may allow savers to truly manage their risk, leave gilts behind and boost income-generating equity allocations.

Paradoxically, by taking the appropriate levels of risk, pension savers may just leave less to chance.

To find out more about DC pensions at Man Group or get in touch, please visit: Defined Contribution Capabilities | Man Group